Central London Net Effective Rents Monitor Q2 2023

The Carter Jonas Net Effective Rents Index

Our Central London Net Effective Rents Monitor illustrates the combined impact of changes to both headline rents and the typical length of rent free periods across 22 central London districts.

The Index also reflects different lease lengths by providing analysis of five and ten year leases, which can have a significant impact on the net effective rent for each district.

Note: the impact of the timeframe for the ingoing tenant to carry out its fitting out works has not been factored into the Carter Jonas net effective rent analysis simply because the timeframe will be influenced by the quantum of space to be leased.

The central London rental cycle

Post-pandemic, much of the central London office market has seen a combination of rising prime headline rents and falling rent free period incentives, driven by low levels of vacancy and a structural shift in demand away from low grade space with a high carbon footprint. Indeed, rent free periods have typically declined by 1 - 3 months for a 5 – 10 year lease since the beginning of 2021.

Importantly, there continue to be wide variations in rental performance between districts, due to differing supply and demand dynamics.

Recent trends – core central London districts

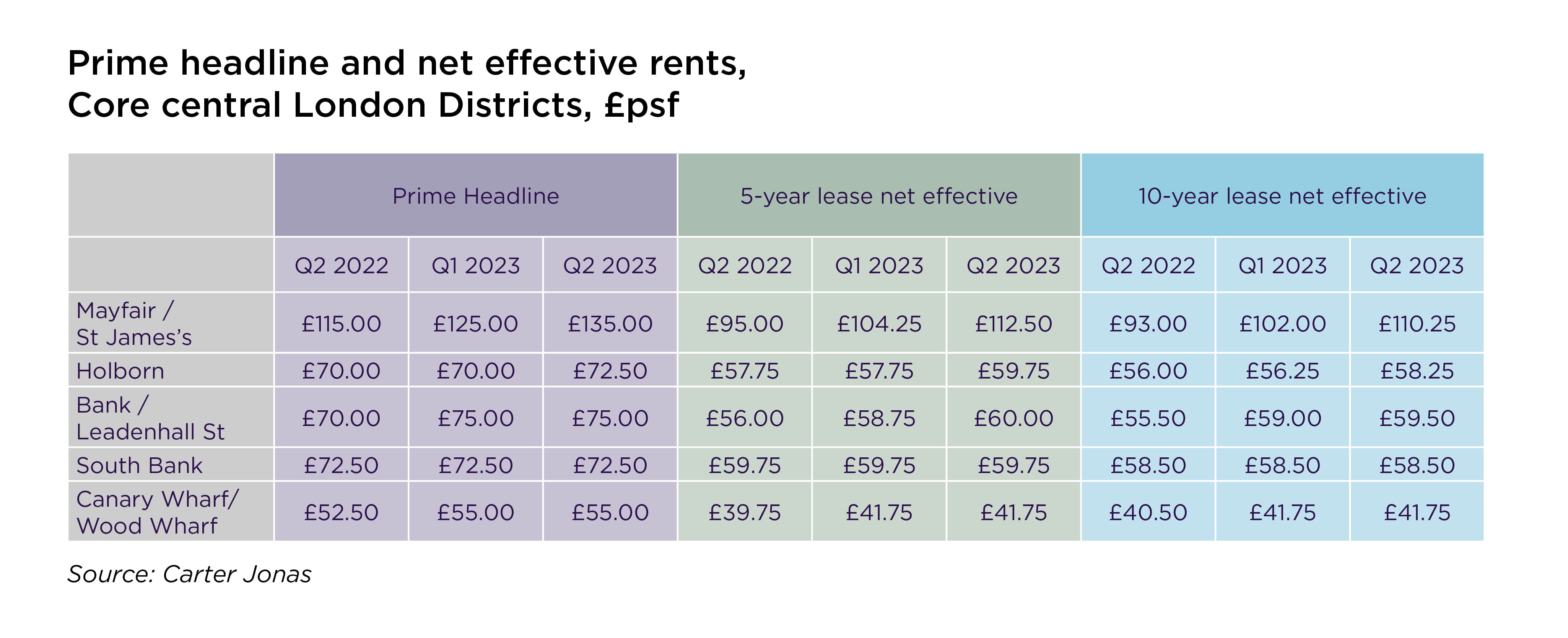

In the West End, an acute shortage of prime space in the Mayfair and St James’s district has seen the headline rent for new grade A space over 5,000 sq ft rise to £135 per sq ft per annum in Q2 2023, from £125 in the previous quarter. This represents an uplift of 8%. Rents for the upper floors of prime-located best in class buildings are now in excess of £180 per sq ft per annum. Over the 12 months since Q2 2022 a combination of rising prime headline rents and a modest reduction in typical rent free incentives has seen the prime net effective rent for Mayfair and St James’s rise by a remarkable 18.6% (for both five and 10-year leases).

In the core Midtown district of Holborn, Q2 2023 saw the prime headline rent move from £70.00 psf per annum to £72.50 per sq ft per annum, a rise of 3.6%. There was no movement in the typical level of incentives in Holborn during Q2 2023.

In the City of London, prime headline rents in the core insurance and banking district around Bank and Leadenhall were stable at £75.00 per sq ft per annum during Q2 2023. However, a shortage of prime stock saw a modest fall in typical rent free incentives during Q2, and the prime net effective rent has therefore increased modestly, by 2.1% (assuming a five-year lease). Over the last 12 months the core insurance and banking district has seen strong annual net effective rental growth of 7.1%.

In Docklands, Canary Wharf/Wood Wharf has performed differently to the other core central London districts, as it is characterised by weaker occupier demand and higher levels of vacancy. Rents and typical rent free periods were unchanged during Q2 2023, which saw the announcement that HSBC is to relocate from its global headquarters from 8 Canada Square at Canary Wharf to Panorama St Paul’s at 81 Newgate Street in the City of London.

Table 1 and Figure 1 show prime headline and net effective rents in the core central London districts.

Trends over the cycle

Figure 2 illustrates how the level of central London prime and net effective rents has moved over the current cycle, using a weighted average across the 22 districts monitored by Carter Jonas. The impact of the pandemic was mainly reflected in rent free incentives, with central London net effective rents falling by 8% peak to trough (assuming a five-year lease), compared with a fall of only 1% for prime headline rents.

Q2 2023 saw a rise in the overall central London prime headline rent of 0.4%, with the prime net effective rent also rising by 0.4% assuming a five-year lease (and at a slightly lower 0.3% assuming a 10-year lease). Over the 12 months to Q2 2023, the prime central London headline rent has increased by 3.0%, with net effective rents rising by a similar 2.9% (for a five-year lease).

Growth in recent quarters means that prime central London headline rents have now fully recovered and are now 2.1% above pre-pandemic levels. Prime net effective rents are now just 0.1% below their pre-pandemic level assuming a five-year lease (and a similar 0.2% below assuming 10 years).

Overall central London rents bottomed out in Q2 2021 (as Figure 2 has illustrated). Figure 3 shows the change in prime headline and 5-year net effective rents across the core districts in the two years from Q2 2021 to Q2 2023.

Very strong rates of rental growth are evident in Mayfair and St James’s, where the shortage of grade A supply relative to demand is most acute. Here, prime headline rents have increased by 22.7% over the last two years, whilst net effective rents (assuming a five-year lease) have risen by an even greater 33.4% as rent free periods have shortened by typically four months on a five-year lease. The other core districts have also seen growth in prime net effective rents, although not as strongly, ranging from 7.6% in the South Bank district to 11.8% in the core City of London.

Key trends - non-core districts

Outside of the core districts, Q2 2023 saw relatively little change in headline rents and rent free periods, reflecting a better balance between supply and demand.

However, a notable exception has been in the Shoreditch / Clerkenwell district on the City fringe where there has been a softening of both headline rents and typical rent free period incentives. These trends have largely been driven by weaker demand from the global tech sector which has a significant presence in these areas due to a combination of higher interest rates, a less certain macro-economic outlook and a relatively high propensity to embrace hybrid working.

In particular, the area around the Old Street roundabout, which has become synonymous with technology businesses, has struggled to secure lettings in recent quarters. This has prompted some developers to reduce rents – typically by at least £5.00 psf. Combined with a small rise in rent free incentives, the prime net effective rent in Shoreditch / Clerkenwell fell by 4.4% in Q2 2023 (assuming a five-year lease).

Outlook

Given the current weak outlook for economic growth, rising interest rates and stubbornly high inflation, occupier demand is likely to be relatively subdued over the coming quarters. Headline rents are likely to be broadly static in most central London districts, and we expect typical rent free incentives for prime stock to increase slightly in those districts where there is still a reasonable choice of quality space. However, for those districts where grade A supply is tight – most parts of the West End and Midtown - headline rents are likely to continue rising for at least the next 12 or so months barring no macroeconomic shocks.

There are notable exceptions to this outlook. In the core West End districts of Mayfair and St James’s, where demand is still strong and prime supply very limited, landlords are now raising advertised rents, and this is starting to translate into transactions being agreed at higher levels. The recent letting of the 86,000 sq ft 36 – 38 Berkeley Square to Chanel, at a rent understood to be in excess of £180 psf, provides an excellent example. In the coming quarters we are therefore likely to see further increases in prime headline rents in the core West End. We also expect to see a ‘ripple effect’ to other West End districts where the choice of high quality buildings available to occupiers remains very limited.

In contrast to the market for prime space, to which this report refers, rent free periods for secondary space with poor environmental credentials have seen little movement over the last twelve months. This is not likely to change, and in many districts, the gap between prime and secondary property is likely to widen further in the coming quarters.

Landlord Advisory for Commercial Properties

Carter Jonas is able to advise landlords across the UK, operating in all sectors of commercial property.

Find out moreOur contributors

© Carter Jonas 2023. The information given in this publication is believed to be correct at the time of going to press. We do not however accept any liability for any decisions taken following this publication. We recommend that professional advice is taken.