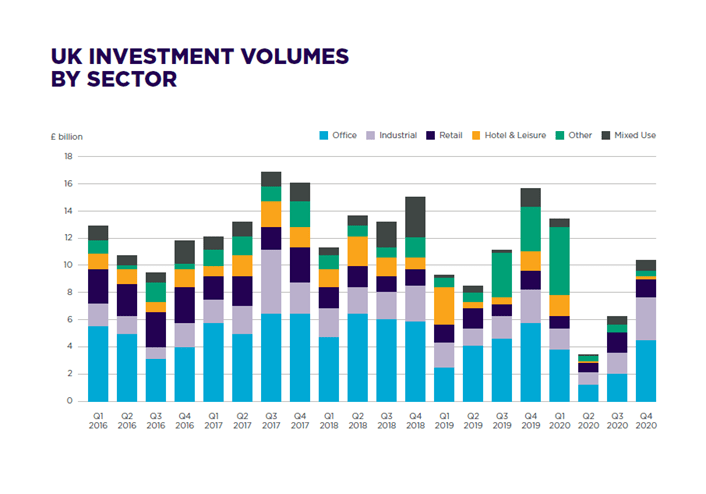

In the office sector, £4.6 billion traded between October and December 2020, comparing favourably against the £2.1 billion invested into the sector during Q3. A total of 13 deals, more than £100 million, were recorded of which nine were in London and 11 were acquired by overseas investors, the largest being Singaporean investor Sun Venture’s acquisition of 1 & 2 New Ludgate in London, EC4 for £552 million from Landsec, generating a 4% net initial yield for the purchaser. Another deal of note was the acquisition of a portfolio of 58 Government offices for £212.5 million by Elite Commercial REIT, a Singapore-based investment trust. The portfolio covers 1.3 million sq ft across the UK, with a third located in London, and generates a gross income of £14.1 million annually.

The industrial sector remains in good stead, with Q4 investment reaching £3.1 billion. Volumes have outperformed the previous quarters of 2020 and are up by a fifth on Q4 2019, reinforcing the continued strong investor sentiment for the sector. The largest deal of the period, the Platform portfolio, was acquired by Blackstone Real Estate from ProLogis UK for £473 million and comprises 4.3 million sq ft across 22 buildings located primarily in the Midlands and across the South West and North West of England and an additional 31 acres of development land. There were four other deals which crossed the £100 million mark, including three national portfolio transactions, and the sale of Electra Park in East London. The latter was acquired by SEGRO for £133 million, generating a 2.58% net initial yield.

Investment in the retail sector continues to reflect the ongoing structural shifts on the high street, which are being accelerated by the pandemic. Despite this, however, the sector has shown some resilience during the final quarter of 2020. Close to £1.5 billion was acquired in Q4, up by 8% over the quarter and 5% on Q4 2019.

Mixed-use and alternative property acquisitions collectively totalled £1.2 billion in Q4, down by about 5% on Q3 and close to 50% below the five-year quarterly average. The quarter’s figure was largely bolstered by the acquisition of the Nova Estate in London, SW1, purchased by Suntec REIT, a Singaporean-based investment trust, for £430.6 million, giving them a 50% interest with the Canada Pension Plan Investment Board. The estate comprises two office and leisure buildings (Nova North and Nova South) and a predominately residential building (The Nova Building) totalling 569,000 sq ft.

The hotel and leisure sector has been particularly hard hit by the pandemic, with only £76.1 million transacted in Q4. Although this is almost double that for Q3, investment is far from the highs seen in previous years – between 2015 and 2019, a quarterly average of £1.5 billion was being achieved. Birmingham was home to the largest deal of the quarter, the £38 million acquisition of 2 Exchange Square by LaSalle Investment Management, with the property anchored by a 235-bed Premier Inn hotel, and including a 6,000 sq ft restaurant and a 5,000 sq ft retail unit. Another deal of note was the £8 million purchase of Lansdown Grove Hotel in Bath by UK-based investor The Axcel Group. The vendors were private individuals, represented by Carter Jonas.