- Date of Article

- Mar 01 2022

- Sector

- Farms, estates & rural leisure services

Keep informed

Sign up to our newsletter to receive further information and news tailored to you.

Capturing the energy locked up in the vast amounts of material that we throw away each day must surely be central to any nation’s energy future. But, as with so many simple solutions to complex problems, the use of energy recovery technology to capture the energy from waste that cannot be recycled is not without its challenges.

Historically the main treatment route for waste in the UK has been landfill, primarily due to the availability of suitable sites created by past mineral extraction. As a result, the UK has historically lagged behind other parts of Europe in its drive to develop and exploit alternative, less environmentally polluting waste management routes.

The process of disposing of waste by incineration has been around since Albert Fryer’s first patented design for the waste “destructor” was constructed in Nottingham in 1874. This new technology was hailed in terms of its ability to manage a growing toxic urban waste problem while also generating vital steam power needed to drive the industrial revolution.

This success meant that the idea quickly spread with similar plants constructed up and down the country. By the early twentieth century, many large towns had their own destructor, which were subsequently renamed incinerators. These were primarily used for waste disposal, with a focus on volume reduction only, as an alternative to landfill. These plants often suffered with incomplete combustion and uncontrolled emissions, with little or no material or energy recovery.

H2: Embracing the new power of energy from waste

The development of energy-from-waste (EfW), energy recovery (ERF) or waste-to-energy (WtE) facilities continued throughout the twentieth century. This energy “recovery” is a step up from disposal, as it involves generating electricity (and, in the case of combined cycle systems, heat) from the combustion of waste.

These facilities are often confused with incinerators and have never really been well received by the public, particularly after it was discovered in the 1960s and 1970s that toxic dioxins were being emitted unchecked from many of these older incinerators.

The regulatory trajectory of the 1990s has ultimately seen the development of sophisticated emissions control systems and the robust regulatory environment that now exists. Thankfully, many of the older facilities closed over that period, but their legacy lives on in the hearts and minds of the public, hindering the adoption of new cleaner technology.

H2: Cleaner tech to meet the climate change challenge

A greater recognition of the potential impact of waste management on climate change in the mid-1990s, principally caused by disposal of waste to landfill, prompted new EU targets for the diversion of biodegradable waste from landfill and the Landfill Tax escalator was born. This has increased year on year, and the charge to dispose of waste into the ground will be £98.60 per tonne from April 2022.

This tax helped drive the development of a new generation of EfW plants that included energy and heat generation in addition to waste management as a key part of their function and business model.

Today, all waste plants using thermal treatment must meet stringent emissions limits, monitoring, waste reception and treatment standards brought in under the Waste Incineration Directive (2000/76/EC), later recast into the Industrial Emissions Directive (2010/75/EU).

H2: The drive towards cleaner energy from waste

For all the effort to embrace a circular economy in which resources are reused and recycled for as long as possible, the amount of unrecyclable waste remains high in the UK. EfW facilities can play an important role in the waste management process by diverting this unrecyclable waste from landfill and turning it in to a useable energy source, not least as the global energy market weans itself off fossil fuels.

In 2020, there were some 55 operational EfW plants in the UK. Despite the technology being highly regulated because of past health concerns, the plants are still seen by the public as bad for air quality, including through the release of dioxins, NOx and ultrafine particulates. The delivery challenge is therefore as much one of communication as it is technology.

For example, and to put dioxin emissions from EfW into context, the Environment Agency has pointed out that the emissions from London's one-minute-long millennium firework display equalled 120 years’ worth of dioxin emissions from the South East London Combined Heat and Power plant, an advanced EfW facility. There have been a number of studies undertaken in recent years which have demonstrated that there is no or negligible health effects on local populations. Public Health England can be quoted as concluding that “any potential damage to the health of those living close by is likely to be very small, if detectable.”

This highlights how operators of modern facilities have made huge investments in advanced emissions abatement technology, developing large-scale facilities, capable of processing approximately 14 million tonnes of UK waste per annum in the UK. These developments have been predicated on large municipal and commercial waste contracts underpinning the funding of their construction, often in excess of £300 million.

Read more: Winning the war on plastic – can an industrial development site on the Manchester Ship Canal hold the key to drastically reducing the UK’s plastic waste problem?

We are now seeing plans for smaller scale “decentralised” ERFs, capable of processing smaller volumes closer to the actual waste arisings and in response to local demand across the country, leveraging pockets of waste where larger facilities may be uneconomic. These plants are looking to alternative recovery technologies to incorporate the production of biofuels and hydrogen for aviation and freight haulage. As such, the communication challenge is likely to only increase and become more complex.

H2: Investing for the future in energy from waste

Years of failure to invest in modern EfW plants means that the UK currently exports approximately 1.5 million tonnes of waste as Refuse Derived Fuel (RDF) and Solid Derived Fuel (SRF) to EfWs in Europe. Rising taxation and shipping costs mean that the argument for investing in the technology to use this “resource” domestically is growing.

Residual waste contains a significant proportion of so-called ‘biogenic’ materials, such as food and wood, from which energy released is considered renewable. However, residual waste can also contain a significant proportion of wastes from ‘fossil’ sources such as unrecyclable plastics. Therefore, when energy is recovered from mixed residual waste, it is often considered only a partially renewable source.

Despite investment to segregate and separate waste streams, the reality is that it is not always possible. Such contamination of waste has a very real impact, reducing overall recycling rates and increasingly tarnishing otherwise highly renewable waste energy sources.

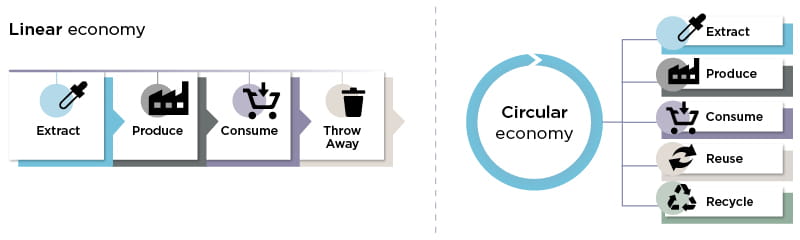

In addition, there is a real concern that any increase in EfW could perpetuate the linear economy (extract-make-consume-discard) and create new barriers to public acceptance of the value of recycling and the development of the circular economy (extract-make-consume-re-use/manufacture/recycle).

H2: Energy from waste: a sustainable energy solution

Clearly, when it comes to waste management, the most sustainable solution is to reduce, reuse and recycle. Disposal must be the last resort and for unrecyclable waste only.

EfW is currently seen as one of the most sustainable ways to treat our unrecyclable waste. While the waste incineration process of course adds to the overall amount of carbon dioxide released into the atmosphere, the ability to divert significant amounts of organic waste from landfill substantially cuts the amount of the more damaging methane contributing to climate change.

Investment must also include optimisation of the existing EfW facilities, through the retrofitting of carbon capture technology and the recovery of heat through heat networks, where possible. On this basis, EfW can be transformed, making a major contribution to decarbonising the UK economy.

The industry has witnessed huge technology improvements and cost reductions in recent years, potentially strengthening the UK’s opportunity to embrace EfW technology further. Yet despite these advances, the industry has struggled to secure the necessary private investment to underpin this technology due to the demise of the Private Finance Initiative, Renewable Obligation Certificates and the reality that long term municipal waste contracts are now largely tied up.

However, new public support now seems likely, as EfW with Combined Heat and Power becomes eligible for government grants in the latest Contracts for Difference (CfD) Allocation Round 4, which is auctioned this year.

H2: Achieving the balanced view

In 2018, the UK processed just over 11.5 million tonnes of residual waste in EfWs (Tolvik Consulting, UK Energy from Waste Statistics, 2020).

Though this sounds a substantial figure, it must be considered in the context of the total waste produced (222.2 million tonnes, according to Defra) – with typically just under 50% of waste being recycled, the volume processed through EfWs was just around 10% of unrecycled waste.

It is a huge opportunity to raise national recycling rates and embrace the circular economy to help accelerate a radical change in the scale and composition of that residual waste.

The government’s net zero strategy is a major driving force behind this change and is likely to have implications on the design of future EfW development. These developments will need to provide opportunities for “tri-generation” – to deliver heating, power and cooling locally where we lag starkly behind the best performing countries in Europe. This can help to boost the competitiveness of local businesses, therefore preserving existing employment and improving energy security.

The challenge of delivering future EfW will therefore certainly increase, requiring investment to support not only the management of waste, heat, and power but also to stimulate and drive the development and expansion of new carbon capture and storage technologies as key to cutting carbon emissions from the EfW.

In a perfect world there would be zero residual waste; but as long as there continues to be, we see EfW to be the most sustainable method currently to treat residual waste, and is much more favourable than landfill.

The reported misgivings are largely a legacy of poor communication, and we see better transparency as the best way to rectify this. EfW, especially with abatement and tri-generation, will play an important role in helping the world decarbonise and transition to a more circular economy.

Despite these considerable challenges, the demand for EfW development will continue, particularly in areas that are able to secure long-term waste supply contracts. Realistically, it is a demand that will only increase as the nation moves closer towards its 2050 net zero target deadline.